Afranga P2P lending platform launched as a bright star and gained popularity amongst investors pretty fast. We have registered and started investing there by ourselves and so far we like what we see. To widen our information about the platform, we have decided to contact its COO Yonko Chuklev with interview inquiry. He responded promptly and as he already knew P2Pforum project, he welcomed the opportunity to introduce Afranga to our community a little bit more.

Hi Yonko, thank you for accepting our interview inquiry. Afranga has gained a popularity quite quickly after its launch amongst our followers, do you see it as a sign of StikCredits good reputation from other P2P platforms? Have your expectations been met in the first months after the Afranga start?

Hi Zbyněk, thanks for the opportunity. Our track record on other platforms has surely helped as for the last three of years investors have seen our performance consistency, business growth and superb crisis navigation. Our expectations with Afranga have actually been surpassed and we are observing greater interest than anticipated. Two months after the start we have over 400 investors and reached a million euro invested on the platform.

What a start! It must make you and your team proud. How does it actually work in the team, is there any connection between Afranga and StikCredit employees? Is the work capacity shared or do you have separate work positions? Additionally, could you introduce yourself, so our readers know your role at the platform?

Afranga and Stikcredit are the same legal entity. Stikcredit has backed the platform with the main company so the market could see the importance of the P2P lending niche and to show that it has the financial firepower to scale the project. Afranga leverages the existing infrastructure of Stikcredit, such as IT, HR, and accounting resources, but we view Afranga as a capsule within Stikcredit that operates autonomously.

I’m the chief operating officer of the company and am dedicated solely to Afranga. I work closely with our senior management, marketing, customer support, treasury, and compliance people. Together we drive the operational rhythm, product development, customer service and growth strategy of Afranga.

Many of our readers know StikCredit from other P2P lending platforms, where StikCredits has been active. Should Afranga be the only exclusive partner in the future, or will StikCredit continue listing loans elsewhere as well?

We will continue our professional relationship with other platforms as we value our partnerships and Stikcredit as a lending company which resorts to external funding to grow its market share needs to have diversified and secure sources of funding. However, Stikcredit’s focus will be on the growth and development of Afranga as a marketplace and the listings on other platforms will likely not be on par.

Ok, what about the vice versa situation – StikCredit is the only lending company at Afranga at this moment. Are you negotiating with others to increase diversity?

We have been contacted by several loan originators and we do plan to list loans from additional companies to increase investor diversification. We’ve just launched, and we are currently focused on improving and fine tuning the internal processes. Once we’ve gained some experience running the marketplace, we will begin onboarding other companies that fit our criteria. We are also focused on bringing product diversity to the platform and we’re discussing with Stikcredit’s management to introduce additional loan products with different risk profile.

Diversification options will be surely appreciated by investors. What about interest rates? Afranga’s offer belong to the highest ones across the P2P lending market. Is it sustainable from the longer perspective or do you see it as a temporary promotional activity to increase the number of investors?

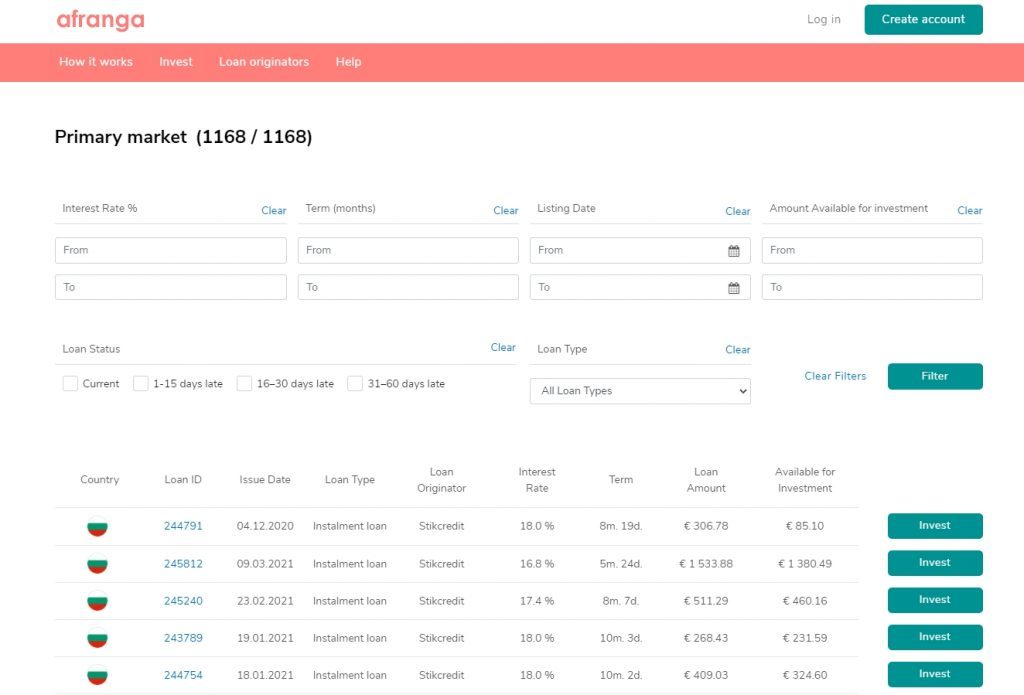

We wanted to reward the early adopters on our platform with higher rates. Occasionally we expect to list loans with interest rates in the strata of 18%, but the main loan offerings are expected to revolve in the range of 14%. Currently loans on Afranga are offered with a return of 16.8% per year.

Secondary market implementation has been mentioned in one of the previous newsletters. Is there any time estimation when it could be introduced?

Implementing the secondary market is surely a big step for our team. We’ve been working hard to make sure everything is tested, proven and functional before going live. We expect to introduce the secondary market in the next 4 – 6 weeks.

Well, that is fast. Your team is definitely not idle. What other news/features prepared for the near future can investors look forward to?

All the features that are in Afranga’s development pipeline are based on the investor feedback we’ve received so far. Such features include an automated tax report, periodic notifications on account statement activity and the ability to download detailed information on one’s investments.

Let’s move to P2P picture from bigger perspective. How do you see the P2P lending sector in Europe? There have been some problems, even frauds, at several platforms. This harms the whole industry. What steps do you consider important to remain transparent in the relationship to investors?

Like every fast-growing industry, the expansion of P2P lending has not been without challenges. The problems we saw with a couple of platforms brought to the surface a lot of deficiencies in terms of market design, poor operational procedures, lack of oversight, and due diligence. On the one hand this truly was a setback for the entire industry, on the other hand it showed the companies in the sector transparency and sustainable growth are essential.

In terms of transparency frequent reporting, timely fulfilment of buyback obligations, skin in the game by each loan originator are necessary. Apart from fulfilment of the obligations towards investors, I believe internal risk management practices are also fundamental. This includes a blend of financial health checks, portfolio quality and performance, operational efficiency, local market condition changes and reputational and AML assessments as well as ongoing analysis of the performance.

Is there anything you would like to say to our readers? Why should they choose Afranga:-)?

I think if someone has to say why your readers should choose Afranga, it should be our current investors. One of our investors said “Afranga implements P2P marketplace features, which have normally taken years in just a couple of months” and another wrote “Your platform is the fastest of all I invest on”. Some of the feedback I’ve seen on P2Pforum.cz includes “shows good reporting with solid results” and “simple design and straightforward control”. This is in line with our understanding that customer feedback and satisfaction are probably the best marketing tool.

That’s an elegant way how to answer:-) Yonko, one last question. What does the name Afranga mean? Is it an abbreviation of some kind or why did you choose it as a portal’s name?

The “Afranga” name was crowdsourced from our team, we believed that this brand can be both catchy, easy to pronounce in many different languages and memorable for investors from all over Europe. The name itself does not hold a specific meaning, but we joked we needed a name with lots of “A”-s, as they stand for “Action” and taking action if what we are constantly focused on, that’s how we came up with Afranga.

Thank you for your time and provided answers. Hopefully we have cleared some topics for P2P investors and we will be looking forward to next Afranga development.

No problem, it has been a pleasure, thank you.

Where to next?

- Afranga official website

- Afranga overview page at P2Ptrh

- Comparison table with more than 30 P2P lending platforms