Before the review itself, let me here thank Cupi, who put the review below together. As you know, I’m active on quite a few platforms myself and just maintaining them and keeping track of other developments is time consuming. Therefore, I do not rush into further registrations. Nevertheless, at the same time we would like to keep bringing new possibilities and expanding horizons to the readers on our website. That’s why I’m glad that we have managed to agree on cooperation with Cupi, who is also active on P2Pforum. It brings a look at other platforms and from a different perspective. You can read what Cupi decided to tell us about himself and his experience in P2P in the short medallion below his article. Zbynhu

Basic information about the platform

The platform is backed by management with more than a decade of experience in the industry. LendSecured, launched in mid-2020, belongs to the Secured Finance MGMT group, which includes other brands such as Lande (media promotion, agricultural loan offer) and mortgage companies Latvias Hipoteka and Atrahipoteka. The group has also received a debt recovery licence. The platform is expected to be renamed Lande in the near future, as it will be merged with the above-mentioned brand. In 2021, the platform applied for a crowdfunding ECSP license (European Regulation on European Crowdfunding Service Providers) in Latvia. However, due to delays from the regulator, the license is not expected to be obtained until later this year.

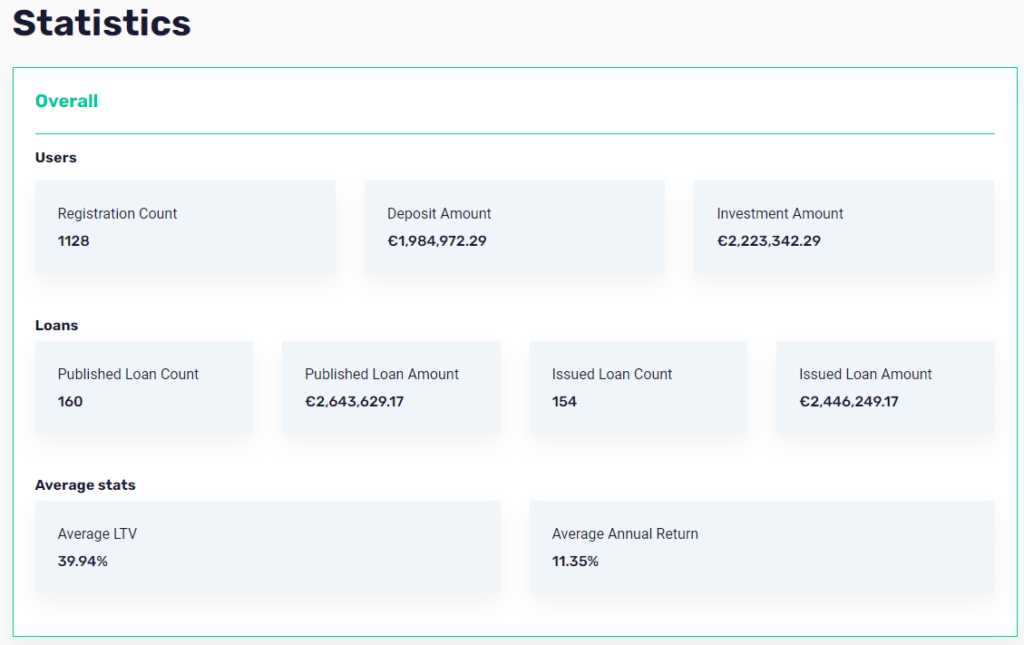

More than 1,100 investors are already registered on the platform, with more than 100 new registrations per month in the last few months. Hand in hand with this and the need to meet investor demand, more and more loans are added to the platform and the share of loans with a higher invested volume is also growing. To give you an idea, a year ago, a EUR 20,000 project was huge and took 10-14 days to be funded by investors. Today, even EUR 50,000 loans are being seen and the speed of funding has increased significantly. To date, EUR 2.1m has been funded on the platform with a current rate of EUR 250-300k per month.

Investing on the platform

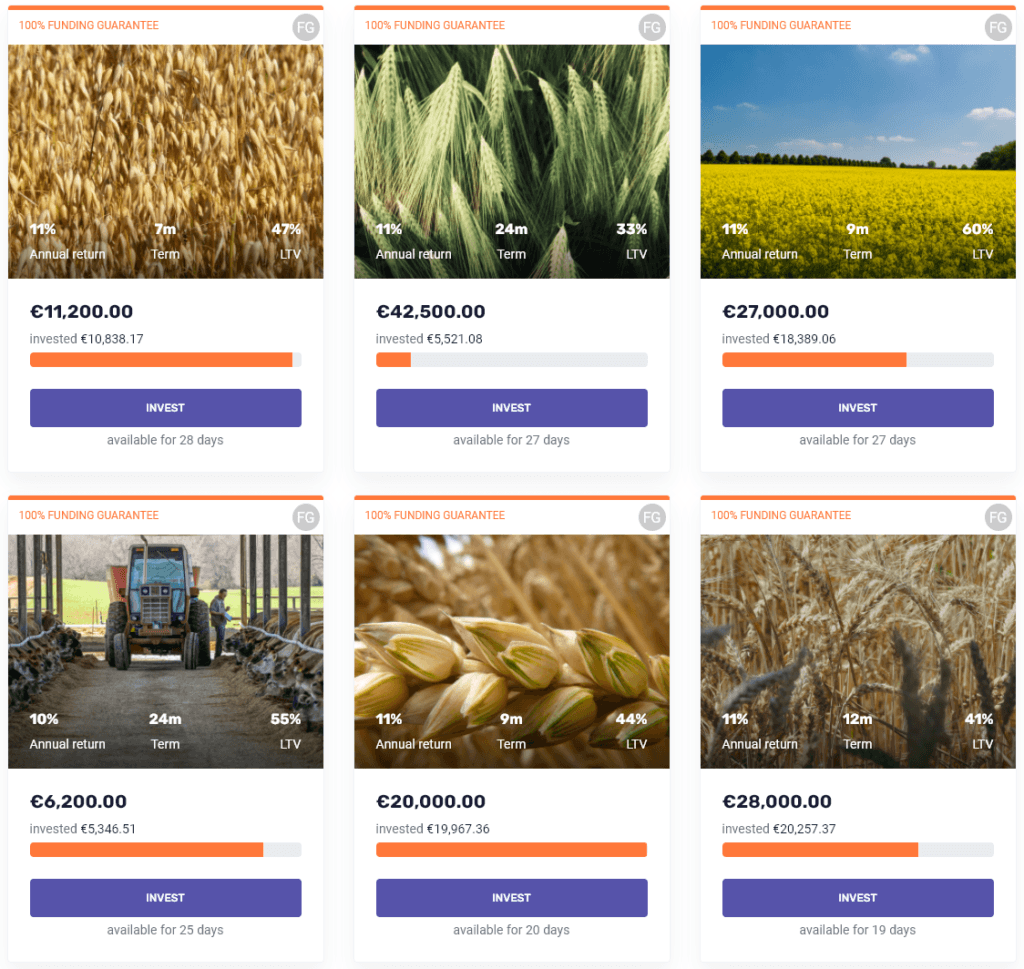

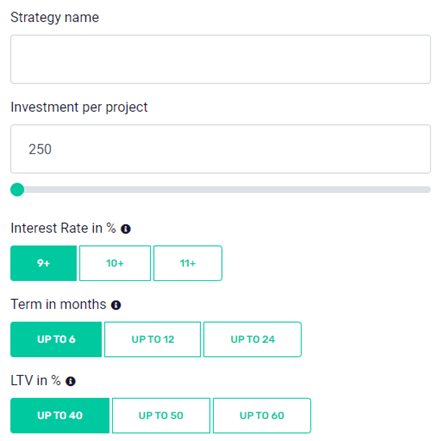

The maturity of the loans offered ranges from 6-24 months with interest rates of 10-11% and an average LTV of 40%. It is the low LTV (Loan To Value) and relatively short-term seasonal loans (6-8 months) that make them an attractive alternative to other platforms for investors. You can also increase your interest rate on selected opportunities with a cashback bonus of 0.5% to 2% on a higher single investment or by using a referral link for new investors.

LendSecured – bonus for new investors

By registering through the link below, you will also support this project.

Auto invest was recently introduced on the platform, unfortunately in probably the most limited version I’ve seen on P2P platforms so far. With an investment between 50 EUR and 250 EUR, there is no way how to set it up, it will just invest in all loans. From EUR 250 onwards you can set the minimum interest rate, LTV and loan term.

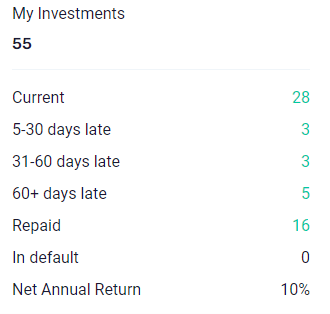

Portfolio statistics after 1 year and subjective experience

The overview of existing investments is probably the biggest hitch in the platform, at least in terms of clarity. The loan designation is just a generated ID, multiple investments in the same loan are displayed separately, and far apart, so you have absolutely no idea how many loans you’ve actually invested in. In general, the platform is easy to navigate, but this is more a consequence of the modest amount of features across the platform. Occasionally inaccurate loan information will appear, probably due to inattention. Unfortunately, it gives an amateurish impression.

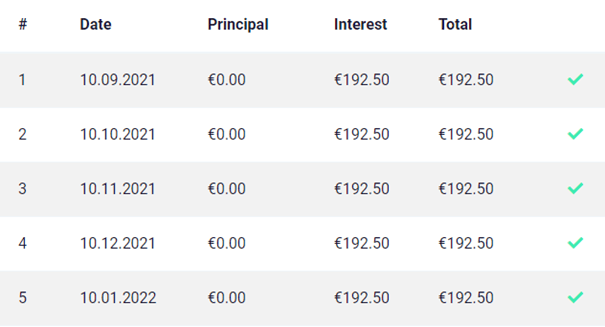

In the platform’s defense, however, I must remind you that it is a relatively young platform (it was only founded in 2020) that is gradually evolving and improving. LendSecured’s programmers don’t slack off, and in addition to the aforementioned auto invest, they feature a nice detail to make things easier, such as a coin icon on the secondary market for loans I’m already invested in, or an exclamation mark icon there for loans in delay. I also appreciate the account statement that you can have generated for any time interval. Here you can see all the information such as net profit, account balance at the beginning and end of the selected period, principal repaid, etc.

Investment safety at LendSecured

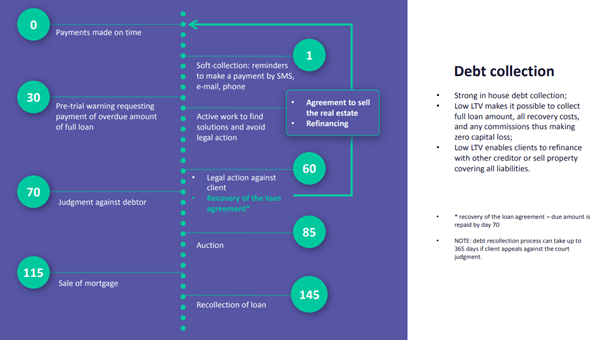

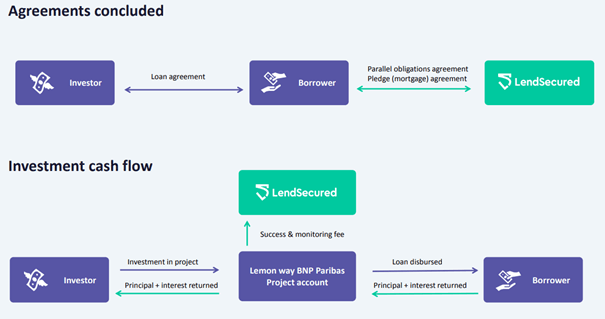

From a safety point of view, it is also important that the money sent to LendSecured sits in your personal segregated bank account with BNP Paribas. This account is automatically set up for each investor and as an investor you don’t have to worry about anything. The LemonWay payment system is used for transactions, however, due to issues with this provider, the platform is looking to agree a different solution for the future. Payments sometimes take several days to reach their destination and this has caused a huge buzz among the investor community. It is a great positive that the management of the platform listens to the complaints and suggestions of the investors themselves.

Platform communication

And while I’m on the subject of communication, management is very active on Telegram (https://t.me/LendSecured). Here you can learn first-hand about new projects on the platform, ask questions to the management or just discuss platform issues with other investors. At the same time, every quarter you can watch a Q&A video on the LendSecured YouTube channel, where the platform’s CEO Nikita Goncars summarizes the events that have happened on the platform, plans for the future, or answers questions from investors.

Review summary – the pros and cons of LendSecured

- Diversification into the new area of P2P loans secured by collateral.

- Low LTV, stable interest rate of 11%, short-term loans offered, secondary market with no premium.

- ECSP license + segregated bank account = higher security for investors.

- Communication, transparency.

- Quality management, history of 100% recoveries on defaulted loans.

- A young platform without a longer history.

- Clarity of some screens, tables, errors in loan descriptions.

- Room for better communication regarding delayed loans.

- Very poor autoinvest setup options.

Conclusion

About the author

My name is Lukáš Cupal and I work as a radiation physicist in the health sector. Since I take voluntary study of anything as a relaxation, I try to broaden my horizons in my free time also in the field of economics and investments. And when I do start something, I go in depth to make it meaningful.

Like many other investors, I jumped into the P2P business in my investment beginnings, mainly due to the accessibility of the platforms to ordinary investors. The riskiness of this business and the need for proper due diligence then motivated me to study financial statements and analysis in depth, which my mathematical heart warmly embraced. It also opened the way to the much larger world of equities.

My curiosity and initial fear then led me to try a lot of platforms, even though none domestic – from Czech Republic. Apart from well-known platforms like Mintos, EstateGuru, PeerBerry or Robocash, I also tried lesser-known platforms like Afranga, Moncera, LendSecured, Debitum Network, EvoEstate or BulkEstate.