In August 2017, I decided to try one of the new P2P investment platforms – Robocash. However, I withdrew my investments in October of the same year – after not agreeing to the new terms and conditions. What finally convinced me to return to the platform this year? In what ways has Robocash moved forward and what is it still lacking in terms of perfection? I have tried to capture my observations in the following review.

Before the review itself, I will mention, that as usual we always review only platforms on which we are active and you can see how our portfolio is doing on a quarterly basis in our P2Preports.

Robocash Group, aka who is behind the platform

The Robocash platform is a typical example of a platform built in-house by a financial lending group operating around the world. Thus, you will not find any provider on the platform that is not under the Robocash Group. This of course brings with it some pros, but also cons (very likely lower backing for investors in case of problems).

Robocash Group was established in 2013 and today operates in the markets of Spain, Russia, Kazakhstan, India (Sri Lanka), Vietnam, Philippines and Indonesia.

However, since the buyback guarantee and the group guarantee apply to all loans indiscriminately, rather than spending time on the detailed selection of sub-providers, it is better to spend time monitoring the performance of the entire group.

Guarantees/obligations for investors, theoretically and practically

The buyback guarantee means that if the loan is more than 30 days past due, the non-banking company buys the investor’s share and adds an amount equivalent to the interest for the entire holding period. With all guarantees – and not just Robocash – but beware. Many newcomers to P2P investing interpret the concept of guarantees to mean that it is virtually impossible to lose money by investing. Each guarantee is only as strong as the one giving it, and so – even though Robocash Group reports good results – it may happen that the provider does not live up to its commitment and investors suffer losses.

A group guarantee means that the individual divisions of the group (countries) within the group guarantee each other’s obligations. Thus, in the event of difficulties in, for example, Vietnam, the members of the group from other countries guarantee the fulfilment of their obligations. However, common sense makes it clear that if, for example, the Russian part of the group, which is the core of the group’s performance, gets into trouble, then the guarantee of the others will hardly be upheld.

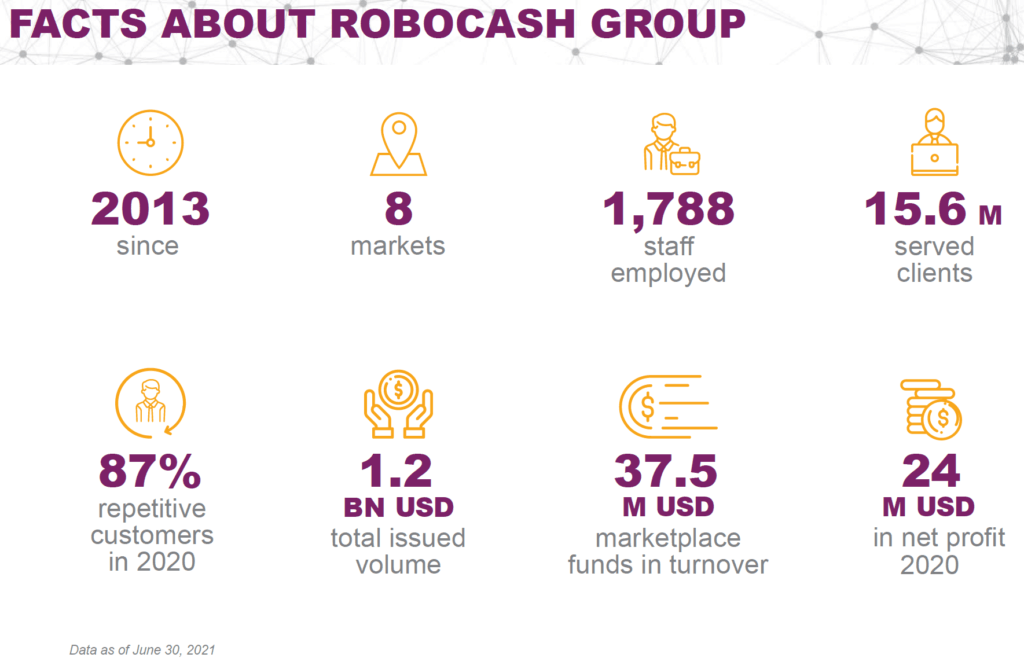

Robocash Group financial results

It must be said that the group is very successful. In the first 6 months of 2021, it generated a profit of USD 14.2 million. Revenues for the same period grew by a staggering 96% to reach USD 144.4 M. This is even more than the revenue for the whole of 2020. Last year’s results have also already exceeded this year’s lending volume – USD 326.5 M (78% increase compared to the second half of 2020).

The group secures most of its funding outside P2P (for example, it recently subscribed to USD 11M worth of bonds on the Moscow Stock Exchange). On its platform, it then raises funding at the level of 12-13% of its loan portfolio.

Robocash regularly presents the results of its platform and the Group as a whole in a web presentation every quarter. It also answers the most frequently asked questions from investors. You can view the full presentation below. I’ll just make a small note here that at the time I wrote the review, the number of views of the presentation was 130. This is desperately low with 18,000+ investors on the platform and indicates that investors are not very interested in their invested funds.

You can find the current statistics of the platform hidden under the About us tab. The financial group regularly reports its results here.

Not a diddly-squat without automation

The basic motto of the entire platform is “Automation above all”. Robocash is built so that the investor enters the basic parameters of the loans he wants to buy, sets up Autoinvest and does not worry further.

Compared to other platforms, the interest rates offered do not change as often (although they do of course reflect the current market situation) and if they do, an informative email is sent to each investor. This way, the investor knows to adjust the Autoinvest settings if necessary and not to accumulate uninvested funds.

The platform goes so far in its “Transfer money to us, turn on AI and do nothing else” approach that manual investing is impossible on Robocash. Indeed, the reasons why someone would want to invest manually are hard to find. In fact, for loans, only the minimum necessary information is disclosed (loan size, length of repayment, nationality of the borrower) and so the investor has no reason to prefer one loan over another.

Secondary market, Loyalty programme

The drive for maximum automation also applies to the secondary market which is available on Robocash. When you sell the purchased loans, you simply click on them and press the sell button. Then you just wait for a counterparty to be found that has the exact parameters of the loans you are selling set up in Autoinvest. The automatic sale will then take place. Manual buying of loans on the secondary market is again not possible.

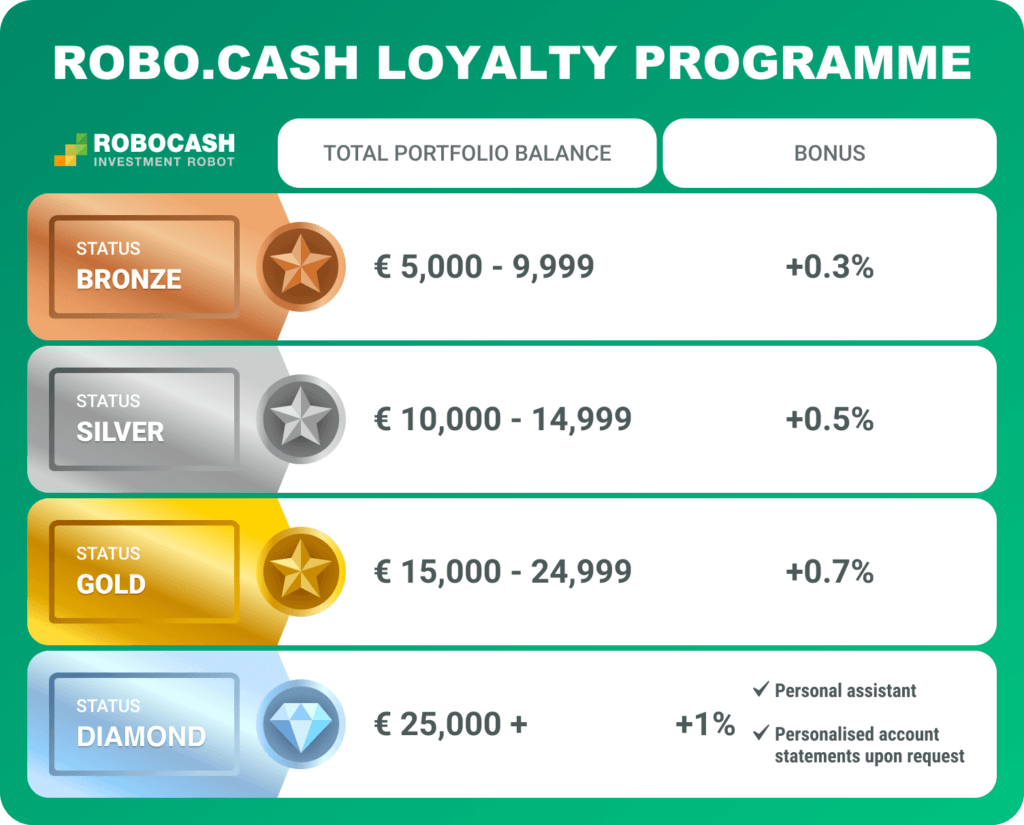

The investor’s inclusion in the loyalty programme is also carried out without any worries. It has four levels and the only criterion that is taken into account is the amount of invested funds. As soon as the investor exceeds the relevant threshold, a bonus label appears in his profile and a bonus rate is added to all further purchased loans.

What to look out for

What makes Robocash different from other P2P platforms is the maximum monthly (or annual) deposit limit. It is set at EUR 15k per month (annual maximum of EUR 180k). The limit is in place to facilitate compliance with AML (anti-money laundering) rules. Smaller investors won’t get any wrinkles from the rule, but it is something to watch out for when trying to transfer larger sums of money.

The second inconvenience you may face is non-cooperating banks.

“Please be informed that AS BlueOrange Bank, which serves our account, does not cooperate with the following banks: Santander Group, ING BELGIUM, Keytrade Bank (Belgian branch), Banco de finanzas, S.A., Hrvatska Narodna Banka. Therefore we recommend you to send funds from another bank account of yours.“

If you have a bank account with one of these institutions and want to invest in Robocash, you have no choice but to open a second account with another bank.

On the contrary, I can reassure those who knew Robocash from the beginning of its existence. Cash drag (or the lack of loans to invest in, and therefore funds lying in the investor account without appreciation) is no longer a problem and there are plenty of loans placed on the marketplace.

Investment strategies

As one of the functionalities that are not common in the P2P field, you can choose a strategy for the portfolio you create. There are 4 options in total, and you can reinvest all funds, reinvest only the principal without interest, collect all returns in an investor account, or have repayments automatically sent to your account. When you turn on this option, you sort of leave your portfolio on a mileage and Robocash will send you funds to your registered account itself every time you accumulate 50 EUR or more. There are no fees for investing on the platform.

Our Robocash portfolio

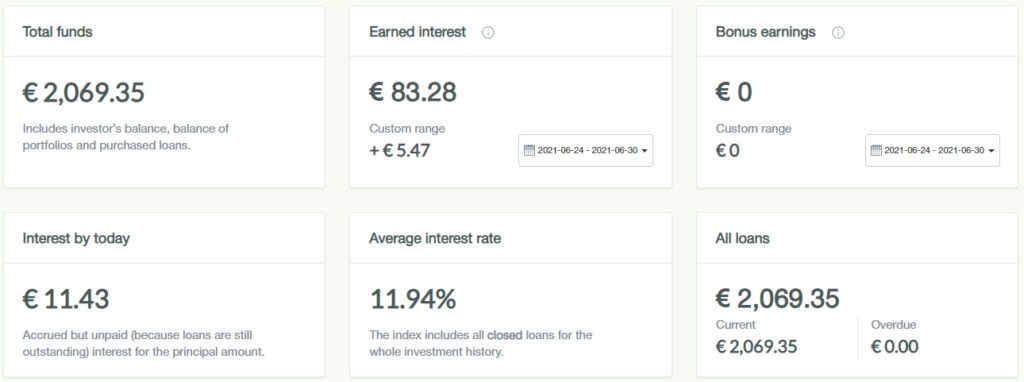

I have only had a small trial amount on Robocash since the beginning of the year without any ambition to increase it. I knew about the platform as a good option to diversify my P2P portfolio and I wanted to keep track of what was happening on Robocash with this amount. However, the summer saw a continued decline in the interest rates offered on Mintos and, in particular, the growth of the non-interest periods there. It’s nice on Robocash that everything is interest-bearing from the date of the investment to its repayment, and this simplicity and transparency is something I like a lot. So I transferred some of my funds and increased my position on Robocash to grab my first loyalty bonus level – +0.3% on each investment.

For comparison I am presenting a screenshot of my portfolio at the end of the first half of the year and now. You can also follow the regular evolution of my portfolio on a quarterly basis in P2Preports.

Robocash bonus for new investors

The Robo.cash platform offers new investors a cashback bonus of 1% of the invested amount for 30 days. To claim the bonus, simply click through the unique link button below.

By registering below you will also support the P2Ptrh project.

Robocash platform – advantages, disadvantages

Advantages

- Full platform automation – almost no maintenance.

- Possibility of diversification to traditional assets or to other P2P platforms.

- Regular and timely reporting of platform and group results.

- Strong Robocash Group behind the platform.

Disadvantages

- Less information on the specific loans offered. The platform is not suitable for micromanaging investments.

- Young P2P lending industry, many relatively unpredictable risks.

- Weaker diversification within the platform (Robocash Group loans only).

Summary

It is no coincidence that Robocash states in its presentation that the typical investor on the platform is a person who has their P2P portfolio diversified among 5 or more platforms. Robocash is actually quite ideal for this. The group behind it has a solid track record, the investing is fully automated, and it has a history to fall back on thanks to its many years of operation. The platform is also so simple to use that it is suitable for those who don’t want to spend their time looking at a number of providers in detail and setting up auto-invests. On the other hand, we wouldn’t choose Robocash as our primary P2P platform ourselves, and we prefer to have it – just like most of the survey respondents – as one of the platforms we are active on.

You can visit Robocash website here.

Other links:

- Afranga: review of young and fast growing P2P investment platform

- Peerberry: review of the growing P2P alternative investment platform

- Robocash overview page on P2Ptrh