Just a year ago at this time, Mintos was being hailed and investors were excited about the “guaranteed” double-digit returns. The year 2020 brought a sobering change, many investors left and some soured on Mintos (or P2P lending in general). What is an objective view of the P2P investment leader? Is it worth investing on Mintos today and does it make sense for a new investor to set up an account on Mintos?

How Mintos works

Every day, already funded loans from lenders are placed on the marketplace and form the offer. The offer is really wide and the numbers of loans available are normally in the hundreds of thousands. From these loans, investors can choose the ones they want to invest in based on a number of criteria (loan type, yield, country, collateral, maturity, etc.).

Since its inception in 2015, Mintos has experienced massive expansion and has managed to grow by hundreds of percent annually. However, in the spring of 2020, at the beginning of Covid-19, the situation took a turn for the worse, with a drastic drop in invested funds as investors started withdrawing their money from the platform. Some providers defaulted, some previously regular on-time payments started to be delayed and communication from Mintos was not the most flexible at first.

Gradually, however, the situation began to calm down and the amount invested started to grow again after stabilization. A big plus is the improved approach of Mintos, which now puts much more emphasis on investor awareness and, for example, regularly holds AMAs (Ask Mintos Anything), where CEO Martins Sulte answers investor questions via sli.do. You can also read the summary of one such session on our website.

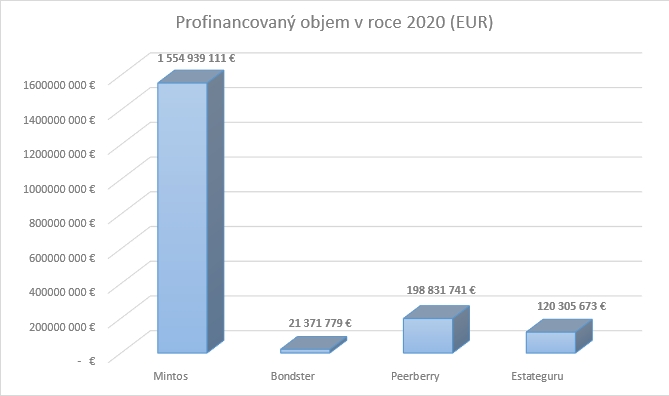

It is also important to mention the fact that despite the decline in 2020, Mintos remains by far the largest P2P lending platform and, for example, in 2020 the growing Peerberry (which is the second largest portal in Europe) still loses a whopping EUR 1.3 billion.

Loan offer on the platform

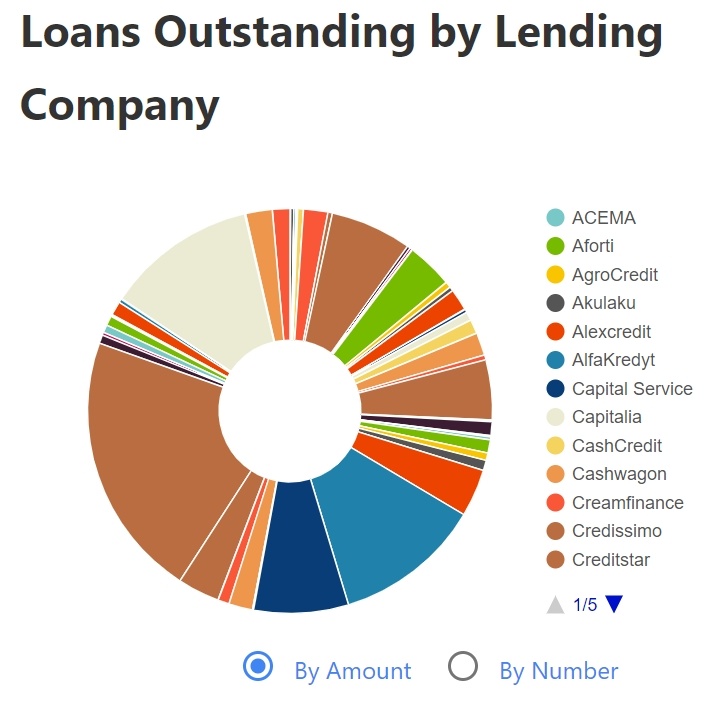

More than 60 lenders offer their loans on Mintos, and you can keep track of what loans are currently on offer and at what yields without registering thanks to regularly updated reports in xls files on the Czech P2Pforum.

The largest portion of loans is available in euros, but you can also buy in rubles, Kazakh tenge, Czech koruna and many other local currencies. All exchanges can be easily converted thanks to the currency converter present on the platform, which works instantly and with only a small fee (depending on the currency pair being exchanged).

If investing on the primary market is not enough, you can also look for suitable loans on the secondary market, which provides liquidity for the invested funds.

Investments can be made from EUR 10 or equivalent in another currency on the primary market. On the secondary market, the minimum amount per loan is EUR 0.1.

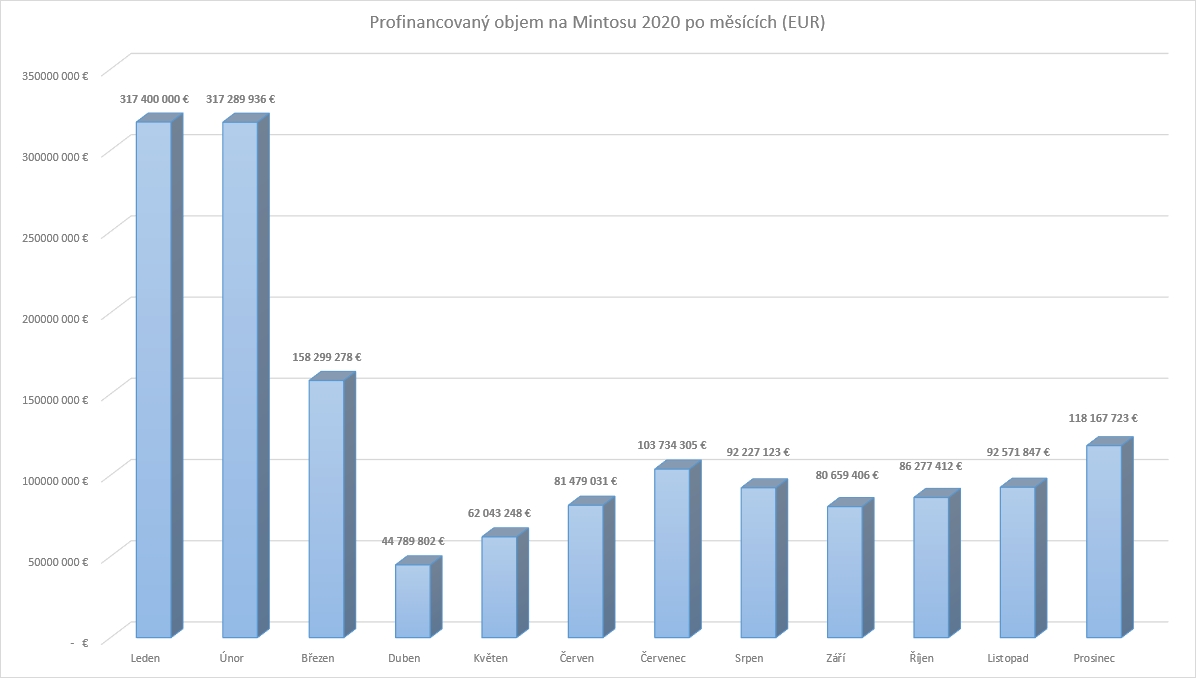

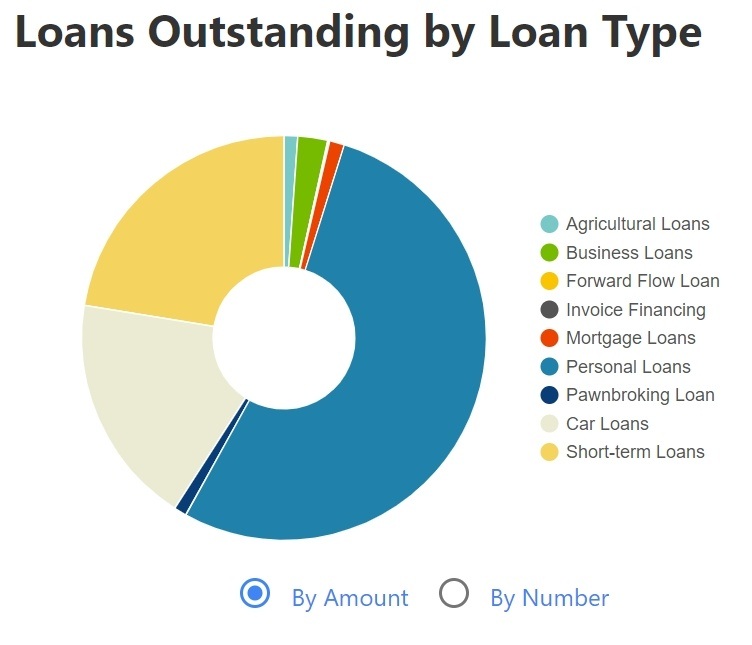

In recent months, the supply of loans on the primary market has been above EUR 200 000, so there is plenty to choose from. The charts below show that there is no shortage of diversification opportunities within the platform.

Mintos investment strategies

Investors can choose from 3 investment methods on Mintos. The decision on how to invest has a significant impact on time, risk and return.

The most convenient, but also the least preferred investment option, is to choose one of Mintos’ predefined strategies. Whether an investor chooses a conservative, diversifying or riskier high-yield strategy, all he or she needs to do is to determine the amount to invest in the chosen strategy. Everything else is taken care of by Mintos itself, which distributes the amount between the providers and the individual loans according to the settings.

For investors who don’t want to be deprived of the freedom to determine exactly what their Mintos portfolio will consist of, Mintos offers the option of autoinvest. You can set up an unlimited number of these, and you can specify in great detail where the free funds are to be invested. For example, investors on P2Pforum make a lot of use of the option to have an autoinvest for each loan originator separately, or even to have more than one autoinvest and for each originator to differentiate, for example, yield or country.

For those who do not want to leave it to the machine or invest according to the specified criteria, there is an option of investing completely manually on a loan-by-loan basis. However, in addition to the time commitment, they also run the risk of having the better-rated loans from higher-rated providers bailed out by the automata.

Loan originators / Lending companies

As an investor could easily get lost in the multitude of providers, Mintos has recently created a simple rating, considering criteria such as financial health, ability to meet obligations, quality of customer service and many others, and has created a simplified numerical Mintos rating. This indicates – from Mintos’ perspective – how solvent the originator is and what risk the investor is taking if he invests to its offering.

From our point of view, this is clearly a commendable initiative. However we definitely recommend basing your decision also on other data such as ExploreP2P rating, monitoring of financial statements or personal interdependence of individual providers. You can also find a lot of information on originators on our website.

We have recently invested mainly in Delfin Group, Iute Credit, Mogo, Wowwo and in Russian rubles in Kviku and Dozarplati..

For those who suffer from decision paralysis and want to have as much information as possible in one tool, we offer the P2Ptrh spreadsheet, where we integrate a range of information on each provider – from Mintos or ExploreP2P ratings to information on group guarantees or grace period lenght.

Guarantee for investors / obligation for originators – theoretically and practically

The concept of P2P lending includes various types of buyback guarantees.

Even on Mintos, you can find a guarantee (now called a buyback obligation for the sake of investor confusion) if the loan is 60 days past due. The non-banking company then rebuys the share from the investor and also adds an amount equivalent to the interest for the entire holding period.

Many beginners interpret the concept of guarantees to mean that it is virtually impossible to lose money by investing. However, any guarantee is only as strong as the company giving it, and so it has happened in the past that the lender has failed to honor its commitment and investors have suffered losses.

For this reason, it also makes sense to do your own research across lenders and perhaps stick to a narrower number of quality companies across platforms. Risks of non-bank P2P lending need to be taken into account and investments divided to different asset classes in terms of diversification. We consider P2P risk to be higher than for equities.

Liquidity on the marketplace

Liquidity on Mintos is ensured by a functional secondary market, where the seller currently pays Mintos a 0.85% fee in the event of a successful loan sale. He can also choose the premium/discount at which he wants to place the loan on the market.

If you decide to sell your participations in times of panic in the markets, you must therefore be aware of the risk of strong competition from “discounted” loans, which may force you to increase your discount and suffer a higher loss. On the other hand, we’ve never seen a loan with double-digit discounts placed on a marketplace for a longer period of time without a successful sale. So liquidity works – the question is whether it’s at a price you’re willing to pay.

If you don’t want to be active on the secondary market, you can choose loans on the primary market with the maturity you prefer. From short-term up to 1 month, to multi-year. However, even here it is not 100% guaranteed that the loan will not be extended (according to the terms and conditions, the lender is allowed to do so up to 6 times for a maximum of 180 days) or on the contrary repaid earlier.

Our Mintos numbers

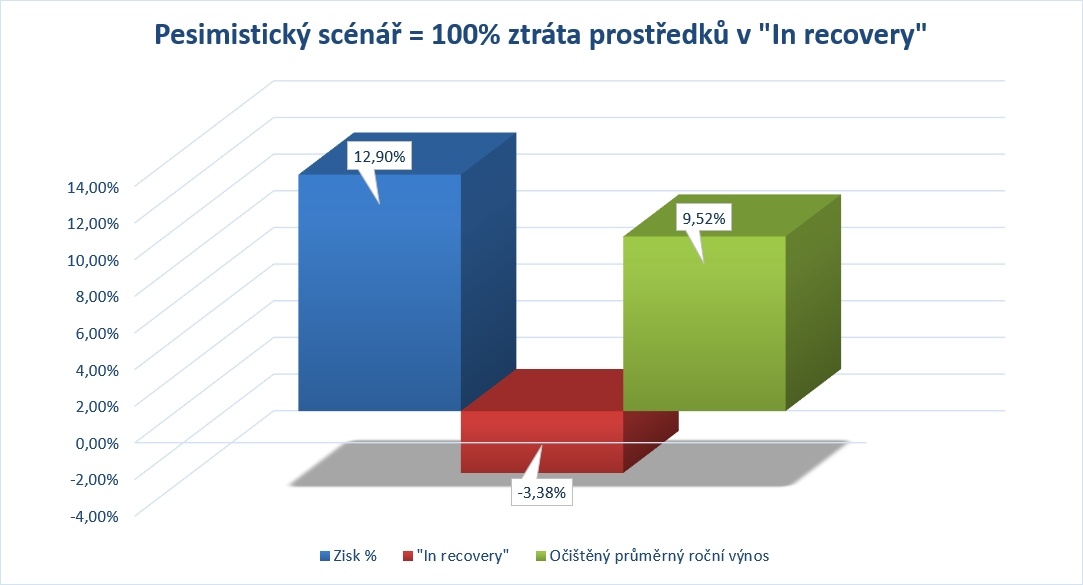

We have been investing on Mintos since mid-2017, giving us an advantage over investors who jumped in later and did not take full advantage of the smooth period of capital appreciation (with the exception of the lender Eurocent). The chart shows our average annual percentage return – calculated in our own excel.

However, it is important to note that the yield in the above graph is distorted by the fact that Mintos has not yet written off some of the lender defaults. The above scenario would only apply if all claims are eventually recovered and investors do not suffer losses. This is unlikely given the number of distressed lenders. This is why we have also prepared a portfolio model where we net the return against the at-risk funds on Mintos stated “In recovery”. In this worst-case scenario, our return drops to 9.52% per annum.

Reálně se samozřejmě budeme pohybovat někde mezi optimistickým a pesimistickým scénářem, průměrný roční výnos by měl překročit dvoucifernou hodnotu. S tím jsme spokojeni, nicméně je na každém investorovi, aby si zhodnotil rizika, která v P2P nejsou malá.

Mintos – investors’ experience

We gather the experience of other investors within the P2Ptrh. We also accumulate other interesting information and links about platforms and non-banking companies, so that a potential investor can get a decent picture in a short time. If you have your own experience with the Mintos platform, we would be happy if you could share it with other investors.

Review conclusion – summary of the Mintos platform – advantages, disadvantages

Advantages

- Market leader with turnover several times higher than its competitors.

- High yield, relatively liquid.

- Wide opportunities for diversification of offers within the platform.

- Possibility to invest with as little as €10.

- Possibility of diversification to traditional assets.

- Functional tools such as autoinvest, secondary market and currency conversion.

Disadvantages

- A young P2P lending industry, a number of relatively unpredictable risks. P2P should be approached as an alternative, to spice up the portfolio.

- After the 2020 experience, one cannot fully rely on the operation and application of guarantees/obligations/warranties. This applies to Mintos and other portals.

- After the introduction of “In recovery” funds, the possibility to extend loans etc., Mintos is a more complex platform for users than some competitors (e.g. Robo.cash, Lendermarket).

- Unless the investor sacrifices a part of the returns and invests through Mintos strategy, investing is not maintenance-free and time is required to manage and maintain the overview.

- 0.85% fee on the secondary market.

Suma summarum

The Mintos platform is a pioneer in P2P investing and dominates the market with its huge variety of lenders and loan types. In the turbulent year of 2020, the platform experienced a massive outflow of investors, but has been able to stabilize the situation, improved communication and some processes. Unfortunately, this has also complicated some procedures.

We continue to invest on Mintos (we are active in euros and rubles). We do not increase or withdraw funds. From our point of view, the yield to date is attractive, and as long as there are no defaults of any of the larger lenders and Mintos manages to cultivate the environment and act transparently, it should easily weather this lean year.

Given its background and expansion, Mintos is a good choice for those who want to try P2P investing. However, don’t believe in 100% guarantees and consider the additional risks that P2P lending brings.

You can check out what the Mintos website looks like here. And if you’re not sure about anything, feel free to drop us a line in the comments below or privately.